Here's where this gets interesting from a momentum perspective. We've covered CTXR before, and you've probably seen what happens when this name gets traction. During previous catalysts, the stock has shown double-digit runs. That performance pattern matters in context of what's actually happening right now structurally.

Current float is approximately 15.2 million shares.

For context, that's genuinely tight. A small float means that when volume picks up and interest shifts, the mechanics of buying pressure work differently than in higher-float names. You get faster repricing, tighter bid-ask spreads as the conversation gets real, and the velocity of information getting priced in accelerates.

Here's what makes this setup particularly relevant: one equity analyst is currently modeling a price target that sits more than 500% above

recent trading levels. That's not fringe research. That's someone with institutional credentials attaching a number that implies significant upside from here. When you combine that analyst perspective with the float structure, the FDA approval just locked in, and the Q4 commercialization clock ticking down, you're looking at a setup where conviction and mechanics align.

The point isn't that the stock will hit that target. The point is that the foundation

exists for quick repricing if commercial execution starts showing and more analysts start upgrading. Small-float biotech stocks with approved products, tight share counts, and fresh catalysts on the horizon tend to move when narrative momentum builds. We've watched CTXR do exactly that before.

Why Now Matters More Than You Think (1)(2)(3)

The window here is specific.

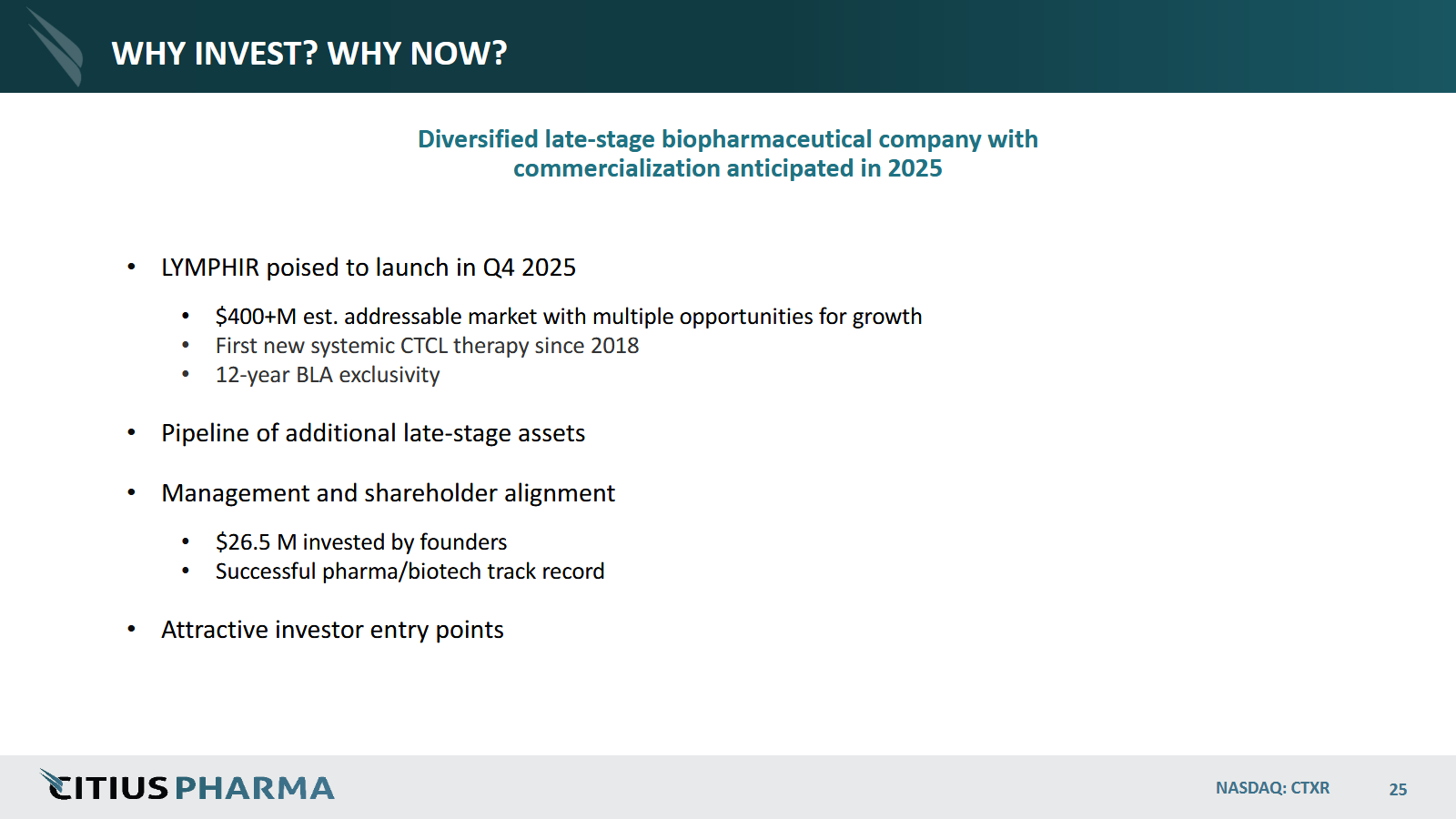

LYMPHIR commercialization is planned for Q4 2025. That's this quarter. Distribution agreements with Cencora, Cardinal Health, and McKesson are already operational. The company has invested in buildout and is moving through the final stages of pre-launch execution.

Here's what retail market participants often miss: the catalysts are stacked for a reason. When a company with FDA approval, manufacturing readiness, cleared distribution, and a Q4 launch timeline enters the final pre-commercial

phase, institutional money starts paying attention. The conversion from regulatory approval to first meaningful revenue numbers creates a narrative inflection point.

LYMPHIR's first full commercial quarter would be Q1 2026, which means investor focus shifts from "will they launch" to "are they capturing market share as expected." That pivot from execution risk to sales trajectory is exactly when momentum stories tend to emerge across small-cap

biotech.

The Real Tension: Execution at Scale 🏗️ (1)(2)(3)

None of this is guaranteed. Biotech launches are messy. Prescriber adoption takes time. Insurance coverage nuances can slow uptake. Manufacturing hiccups happen. Patient awareness campaigns miss sometimes.

But here's what's factually true: Citius has moved past regulatory uncertainty. The company has

already validated the clinical profile. The company has already secured the reimbursement code. The company already has the infrastructure contracts in place. The only variable left is execution, and with management owning $26.5M of their own equity, there's aligned incentive.

Where This Lands 🛩️ (1)(2)(3)(4)(5)

You're looking at a late-stage biopharmaceutical company moving

from approval phase into commercial phase, with a differentiated first in class therapy in an undersupplied market, plus a late-stage pipeline that keeps the story moving even if one asset underperforms.

The peak information asymmetry happens before the street starts covering the commercial ramp in real time. That window is compressed into the next 90 days.

A small float. An analyst target that's 500%+ away. A history of double-digit runs on catalysts. An

FDA-approved product launching this quarter. First in category in seven years. A market that's been starving for options.

We've watched CTXR move on less.

We'll be watching this closely, and we wanted to make sure you had the core facts in front of you before the narrative starts shifting in the broader market.