(4)

The kind of grades that turn geological reports into acquisition targets.

And that's just the silver. The gold discoveries at Homestake Ridge are equally staggering: (4) 🌟

→ 46.31 g/t Au and 70 g/t Ag over 25.0m - that's pure bonanza grade

→ 12.23 g/t Au and 84 g/t Ag over 34.93m - extraordinary width for such high grades

→ 11.80 g/t Au and 1,824 g/t Ag over 9.16m - both precious metals in abundance

These aren't anomalies.

They're finding new high-grade zones all across the property with 2024 discoveries including: (4) 🔍

→ Moose Vein: 977 g/t Ag over 5.00m including a stunning 3,670 g/t Ag over 0.79m

→ Chance Vein: 206 g/t Ag over 23.03m including 597 g/t Ag over 1.40m

This momentum isn't just rare. It's the kind that creates wealth for those positioned before everyone else realizes what's

happening.

The smart money clearly sees what's coming:

- Hecla Mining (America's largest silver producer) has upped their stake to 12%

- Legendary resource backer Eric Sprott holds 9.9%

- Major institutions make up 52% of ownership, including Fidelity

This isn't random interest.

It's calculated positioning ahead of

what appears inevitable.

The Golden Triangle has seen over $5 BILLION in M&A deals since 2018.

Giants like Newmont and Newcrest aren't just watching. They're actively consolidating.

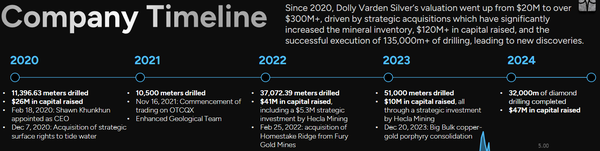

And now consider this: Dolly's 163 km² package is one of the LAST large, standalone high-grade projects still available. (4)

They're sitting in the middle of a corporate acquisition wave with exactly what the majors need:

- Exceptional grades that are becoming increasingly rare globally

- Expandable resources with every new drill result

- Secure jurisdiction in mining-friendly British Columbia

- Strong local relationships including with

First Nations (1/3 of the exploration team is from the Nisga'a Nation) 🤝

- Management that delivers without drama

What's more, this ground has produced before — and not just a little: ⚡

- 20 million ounces of silver have already been produced historically

- The Dolly Varden Mine averaged 1,100 g/t Ag starting in 1919

- Torbrit produced 18M oz at

466 g/t Ag during the 1950s

Meanwhile, larger market forces are accelerating:

- Solar panel demand requires unprecedented silver supplies

- Electric vehicles are consuming more silver than ever

- Global silver supply is running a deficit of 215 million ounces

- Only 13 primary silver companies left globally in the entire world

Now, add Dolly

Varden's recent NYSE American listing — trading as DVS since April 21st — and the perfect scenario is already unfolding:

- Access to the world's deepest capital pools now fully secured

- Dramatically increased visibility with U.S. backers happening in real-time

- More liquidity, more momentum, more institutional coverage building daily

What also sets DVS apart is its exceptional

infrastructure: 🚦

- 25km from tidewater access at Alice Arm

- 30km from power grid and the town of Kitsault

- 46km from deep-water port of Stewart

Simply put: Dolly isn't just sitting on treasure underground. They're positioning for a major re-rating above ground.

The most exciting part? They're exploring the

potential connection between deposits — testing whether Wolf and Torbrit/Kitsol zones might be part of an even larger mineral system. 🧩

Management's aggressive approach speaks volumes.