These results came just weeks after the Pentagon committed $400M to MP Materials to secure U.S. rare earth supply.

The parallel? Governments are no longer waiting for the market—they’re funding supply chain resilience. ATLX, with exposure to REEs, graphite, and titanium through ACM, now plugs into that narrative.

- Definitive Feasibility Study Filed

(DFS) (3)

On August 4, ATLX published its DFS for Neves. Highlights:

- After-tax NPV: $539 million

- IRR: 145%

- Payback: 11 months from start of production

- Opex: $489/tonne concentrate, among the world’s lowest

This DFS isn’t a wish list—it comes after

a mining concession granted May 27, 2025, and the delivery of a pre-assembled processing plant. (3,6)

Together, these milestones compress the timeline to cash flow.

🇧🇷 The Lithium Land Advantage (3)

- 208 square miles of mineral rights — largest footprint in

Brazil among listed players

- Brazil ranked #5 globally in lithium production in 2023

- Brazil’s lithium output is rising quickly as new projects ramp up

- Phase 1 target: up to 150,000 tonnes/year of spodumene concentrate

- Phase 2: doubles to 300,000 tonnes/year

Brazil is rapidly scaling as a lithium export hub, and ATLX holds the single largest exploration

footprint.

🏗️ Plant Delivered and Ready (6)

In March 2025, ATLX completed delivery of its Dense Media Separation (DMS) plant:

- 141 containers, pre-engineered and fully assembled

- Rapid deployment design cuts months off commissioning

- Sustainable processing tech minimizes water and reagent use

This is a

major de-risking step. Investors often discount juniors until they see real steel on the ground. ATLX has delivered — literally.

🤝 Strategic Global Partnerships Secured

- Mitsui & Co. (Japan): $30M equity investment + offtake rights: 15,000 tonnes Phase 1 and 60,000 tonnes/year Phase 2… Berkshire Hathaway is a significant Mitsui

shareholder. (9)

- Chengxin & Yahua (China): ~$50M in combined equity + prepayments, locking in ~80% of Phase 1 production (120k tpa). Both supply lithium directly to Tesla and BYD. (10)

The takeaway? ATLX has already secured long-term customers across Asia. Supply is effectively spoken for before production

has even started.

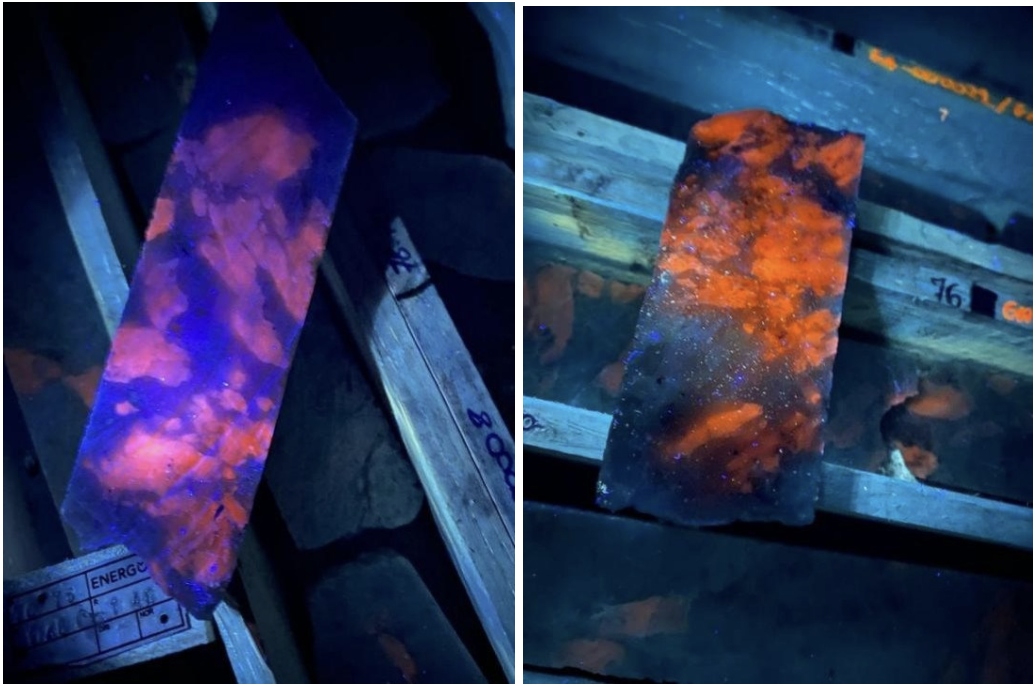

🔁 Atlas Critical Minerals Upside (4,7)

ATLX’s ~30% stake in ACM brings optionality beyond lithium. ACM controls projects in:

- Rare Earths

- Titanium

- Graphite

- Uranium

- Nickel

- Copper

- Iron Ore

- Quartzite

- Gold

This isn’t dilution—it’s a free upside kicker. The market may

value ATLX as a lithium story today, but ACM’s results (like July’s assays) provide a pipeline of future catalysts across critical minerals.

📊 Analyst Coverage & Market Momentum

- Roth MKM: $20 target — over 3x current levels. (5)

- H.C. Wainwright: $19 target, citing strong project economics. (5)

Seeking Alpha: Flagged ATLX for top growth metrics, citing “A+ for growth, A for profitability, and improving revisions.” (8)